For investors, the message is clear. The next decade of infrastructure investment will be defined not only by volume, but by where and how capital is deployed. Emerging markets represent the largest share of future infrastructure demand, the fastest growth rates, and some of the most compelling long-term opportunities—provided risks are appropriately structured and mitigated.

For policymakers, the priority lies in creating stable, investable environments that align infrastructure planning with climate resilience and energy transition goals. Clear regulation, credible transition pathways, and effective public-private collaboration will determine whether projected investment translates into durable, inclusive growth.

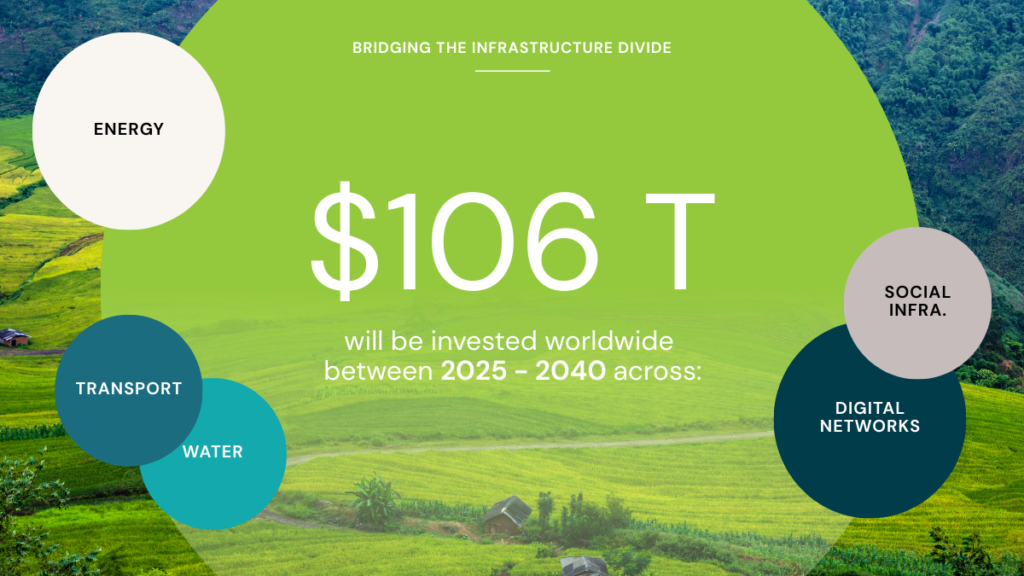

As global capital mobilises toward infrastructure at unprecedented scale, the convergence of climate finance, infrastructure gaps, and emerging-market growth defines a generational investment challenge—and opportunity. Bridging this divide is no longer optional; it is central to economic stability, climate outcomes, and long-term value creation.